(A CEO-Level Guide to Legal Fundamentals, Risk, and Strategic Protection)**

Introduction: Why CEOs Cannot Ignore the Legal Side of Life Insurance

Life insurance is often treated as a personal or emotional purchase—something handled quietly, delegated to advisors, or addressed once and forgotten. For a CEO or business owner, that mindset is dangerous.

Life insurance is not just a financial product. It is a legal contract, governed by laws that determine:

- Who gets paid

- When payment occurs

- Whether a claim can be denied

- How proceeds are taxed

- How insurance interacts with business agreements, estates, and succession plans

At the executive level, misunderstanding the legal foundations of life insurance can expose families, companies, and shareholders to unnecessary risk.

This article provides a layman-friendly but CEO-grade introduction to how life insurance works under the law—without legal jargon, but with strategic clarity.

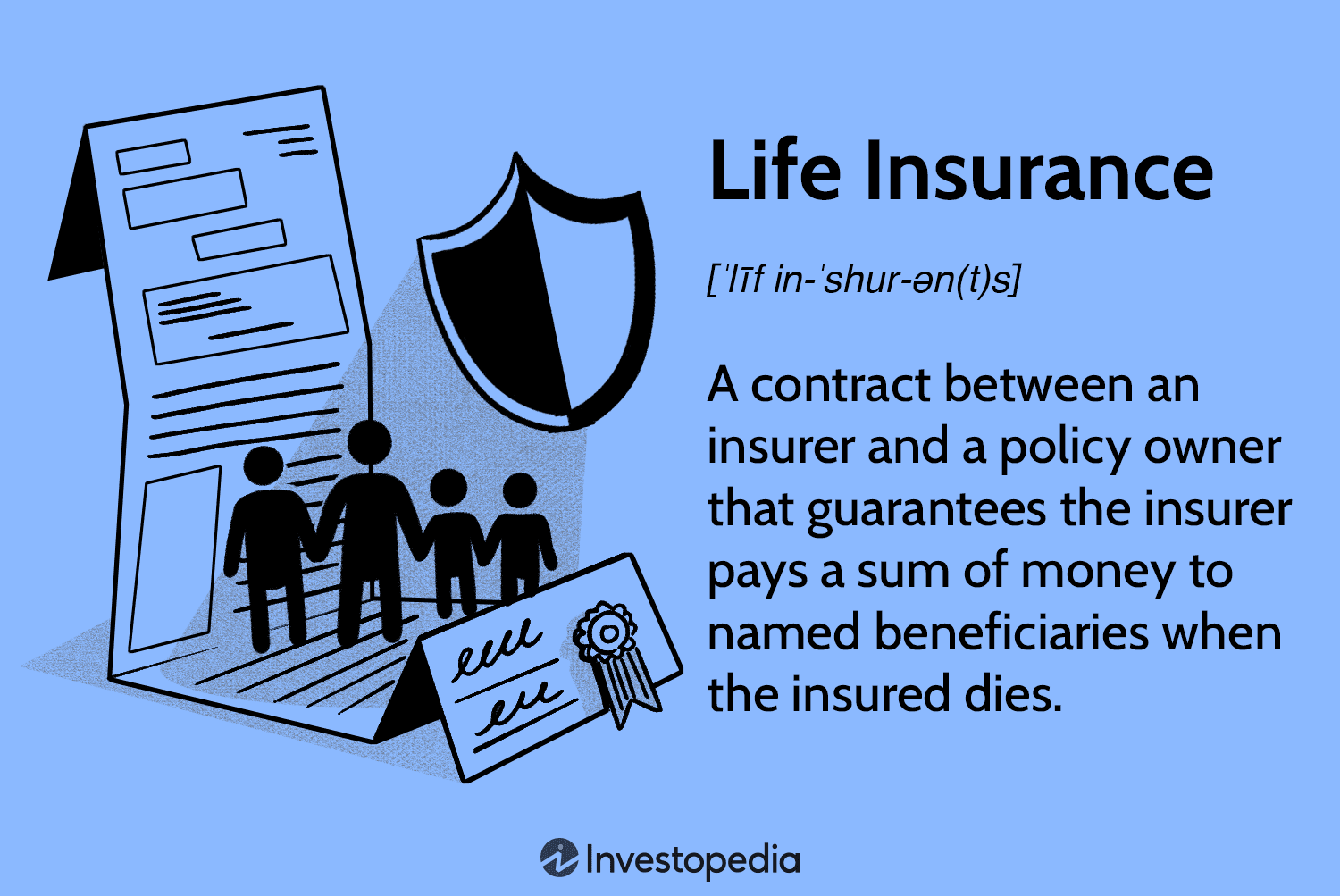

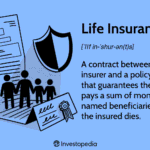

1. Life Insurance Is a Legal Contract First, a Financial Tool Second

1.1 The Core Legal Nature of Life Insurance

At its core, life insurance is a binding legal contract between:

- The policyholder

- The insurance company

The insurer agrees to pay a defined sum of money upon the insured’s death if—and only if—the contract’s conditions are met.

This means:

- Rights and obligations are enforceable in court

- Language in the policy matters

- Verbal assurances do not override written terms

For CEOs accustomed to contracts, this should feel familiar—yet many treat insurance contracts with far less scrutiny than commercial agreements.

1.2 Why “Layman Understanding” Is Not Optional

Executives often rely on:

- Brokers

- Agents

- Financial advisors

While these professionals play a role, legal responsibility does not transfer. If a claim is denied, the insurer will rely on the written policy—not the sales presentation.

Understanding the legal basics is not micromanagement. It is governance.

2. The Key Legal Parties in a Life Insurance Policy

2.1 The Policyholder

The policyholder:

- Owns the contract

- Controls beneficiaries

- Pays premiums

- Can modify or cancel the policy

In business contexts, the policyholder may be:

- An individual

- A company

- A trust

Ownership determines legal control, not who is insured.

2.2 The Insured Person

The insured:

- Is the individual whose life triggers the payout

- Does not have to be the policyholder

Example:

A company can legally insure a CEO, provided it has an insurable interest.

2.3 The Beneficiary

The beneficiary:

- Receives the proceeds

- Has legal standing to make a claim

- May override wills in many jurisdictions

Incorrect beneficiary designations are among the most common legal failures in executive insurance planning.

3. The Legal Concept of Insurable Interest

3.1 Why the Law Requires Insurable Interest

To prevent speculation on human life, the law requires insurable interest at the time the policy is issued.

Insurable interest exists when the policyholder would suffer:

- Financial loss

- Economic harm

- Legal liability

upon the death of the insured.

3.2 Insurable Interest in Business Settings

Examples include:

- Companies insuring key executives

- Partners insuring each other

- Lenders insuring borrowers

Without insurable interest, a policy can be declared void, regardless of premiums paid.

4. Disclosure and the Legal Duty of Utmost Good Faith

4.1 Life Insurance Requires Full Disclosure

Life insurance contracts operate under the principle of utmost good faith.

This means the applicant must disclose:

- Medical history

- Lifestyle risks

- Material facts affecting underwriting

Failure to disclose—even unintentionally—can result in claim denial.

4.2 Why CEOs Must Be Especially Careful

Executives often:

- Travel frequently

- Experience high stress

- Engage in high-risk activities

Omitting or minimizing details exposes beneficiaries to legal disputes later.

5. Misrepresentation, Non-Disclosure, and Legal Consequences

5.1 The Difference Matters Legally

- Innocent misrepresentation: honest mistake

- Negligent misrepresentation: careless omission

- Fraudulent misrepresentation: intentional deception

The legal remedy differs, but all can affect payout eligibility.

5.2 Contestability Periods

Most jurisdictions allow insurers to contest policies within a defined period (commonly 2 years).

After this period:

- Claims are harder to deny

- Fraud may still invalidate coverage

Executives should treat the early years of a policy as legally sensitive.

6. Beneficiaries, Wills, and Legal Conflicts

6.1 Insurance Proceeds Often Bypass Wills

In many legal systems:

- Life insurance proceeds are paid directly to named beneficiaries

- They do not form part of the estate

This can override:

- Wills

- Family expectations

- Succession assumptions

6.2 Common Executive Mistake

Failing to update beneficiaries after:

- Divorce

- Remarriage

- Business restructuring

This creates predictable legal disputes—and reputational damage even after death.

7. Life Insurance and Estate Law

7.1 Estate Liquidity and Legal Timing

Estates often face:

- Immediate tax liabilities

- Delays in asset distribution

- Court processes

Life insurance can legally provide instant liquidity, but only if:

- Ownership is structured correctly

- Beneficiaries are properly designated

7.2 Trusts and Advanced Legal Structures

High-net-worth individuals often use:

- Insurance trusts

- Irrevocable structures

These can:

- Reduce estate tax exposure

- Control payout timing

- Protect beneficiaries

However, they introduce legal complexity requiring professional oversight.

8. Business Law and Corporate-Owned Life Insurance

8.1 Key Person Insurance

Legally used to:

- Compensate for loss of leadership

- Stabilize cash flow

- Protect lender confidence

Ownership and beneficiary designation must align with corporate law.

8.2 Buy–Sell Agreements

Life insurance often funds:

- Shareholder buyouts

- Partnership transfers

If policy terms conflict with legal agreements, litigation is almost guaranteed.

9. Tax Law and Life Insurance

9.1 General Tax Treatment

In many jurisdictions:

- Death benefits are income-tax free

- Premiums are not deductible

- Cash values may be taxable

However, structure determines outcome.

9.2 Cross-Border and Executive Mobility Risks

For global CEOs:

- Jurisdiction matters

- Tax residency matters

- Policy location matters

A legally valid policy in one country may face unexpected taxation in another.

10. Regulatory Oversight and Consumer Protection

Life insurance is heavily regulated to ensure:

- Solvency of insurers

- Fair claims practices

- Disclosure standards

Executives should:

- Choose regulated insurers

- Understand dispute resolution mechanisms

- Avoid unregulated offshore structures unless legally advised

11. Claims, Disputes, and Litigation

11.1 Why Claims Are Denied

Most denials arise from:

- Non-disclosure

- Lapsed policies

- Beneficiary disputes

- Policy exclusions

Understanding these legal triggers reduces risk.

11.2 CEO Best Practice

- Keep documentation organized

- Communicate policy details to trusted parties

- Review policies annually

12. CEO-Level Best Practices for Legal Safety

- Treat insurance like any major contract

- Separate sales advice from legal review

- Align insurance with corporate and estate documents

- Update beneficiaries regularly

- Document intent clearly

Insurance should support strategy—not undermine it.

SEO Keywords (Suggested)

Primary

- Life insurance and the law

- Life insurance legal guide

- Life insurance explained for executives

Secondary

- Life insurance legal issues

- Beneficiary law life insurance

- Corporate life insurance legal structure

Conclusion: Law Turns Insurance Into Strategy—or Risk

Life insurance without legal understanding is not protection—it is exposure.

For CEOs and business leaders, the law determines:

- Whether coverage works

- Who benefits

- How smoothly transitions occur

You do not need to be a lawyer to manage this risk.

You do need clarity, structure, and discipline.

Insurance is not about death.

It is about control, continuity, and certainty.

And those are leadership responsibilities.

Word Count:

974

Summary:

This article is an introduction to the regulatory and legal aspects of buying Life Insurance which the layman should find interesting and useful. Special reference is made to buying life insurance on the Internet.

Keywords:

life,insurance,law,fsa,compliance,adviser,broker,execution

Article Body:

There are no laws in the UK that require a person to have life insurance. It�s an entirely voluntary insurance. About 40% of the UK’s working population are covered by life insurance either through their own policy or via an arrangement through their employer.

So the simple things first. You have to be a UK resident in order to buy a life insurance policy from a UK based insurance company. This is not a requirement laid down in UK law, but UK laws and tax arrangements make it impossible for a UK based insurance company to offer insurance to anyone other than a UK resident. But be aware that if, having taken out life insurance, you later live abroad, your policy will be invalidated. Naturally, invalidation does not apply if you are on holiday but if you have a short-term work assignment abroad you are well advised to inform your insurance company before you go.

All UK Insurance Companies are subject to UK Corporate Laws. However, there are special regulations that only apply to insurance companies. These control the value of the risks the companies take on in relation to their financial reserves. These regulations are designed to ensure that your insurance company will be in a position to pay if you claim.

The Data Protection Act 1998 is concerned with way all UK businesses store, safeguard and use the data they collect about people. This is particularly important within the life insurance industry as the companies store significant amounts of very personal information about you � including your age, health record and life style. One of the key provisions of the Data Protection Act says that if a business wishes to pass on your information for marketing purposes, the business collecting the data must tell you of its intention and give you the opportunity of refusing permission for your data be used in that way. Incidentally, all reputable web sites selling life insurance will have a �Privacy Statement� which tells you how they handle your information and how it is used.

The Financial Services and Markets Act (2000) is the most important piece of legislation affecting the promotion of financial services in the UK including life insurance. The Act is highly complex but is primarily concerned with protecting you the customer. The implementations of the Act is overseen by the Financial Services Authority (FSA). The FSA regulates all forms of the promotion of financial products and services including the activities of financial and mortgage advisors in the UK. Their aim is to ensure you receive clear professional advice that reflects your personal circumstances. They also ensure you have a route to compensation should it be proved that you received inadequate or poor advice.

For the layman, the FSA’s biggest impact is reflected in the advisors they talk to. The FSA seeks to ensure that all financial advisors are trustworthy and competent which includes being well supervised and well trained, and that any advice is given in your best interests. The FSA also ensures that you are given full and accurate information about the products you are being advised to buy both before and after you have bought them. They also closely oversee the organisations that actually create the financial products.

In fact everyone and every organisation giving financial advice in the UK must be authorised by the Financial Services Authority.

However, the Act makes a distinction between financial products bought as a result of a recommendation from a Financial Adviser and �Execution Only� business. Execution Only is where a customer is wholly responsible for the selection of the investment and therefore the financial advisers’ sole responsibility is to process the purchase efficiently. Under Execution Only, the Adviser bears no responsibility for the products suitability for the clients needs.

You should be aware that many of the web sites promoting life insurance operate on this Execution Only basis. However, most web site operators provide extensive information to enable the client to make an informed choice. Sometimes the information is published on the web site and sometimes provided during a follow-up telephone call. Either way, within their Terms of Business the web site will have to tell you on what basis they provide financial services and as part of your application, you will normally be required to confirm that you have read those Terms.

Those Terms of Business will always include details of a complaints procedure. In outline, if a customer wishes to complain, then the customer must detail the complaint in writing and send it to the Compliance Officer for the business employing the advisor. That business then has to investigate the complaint and reply to the customer in writing. If the Compliance Officer upholds the complaint, and the customer has suffered a financial loss as a result, then the business must agree a financial settlement with the customer. Ultimately, if the customer has suffered financial loss and cannot accept either the organisations� conclusions or their proposed financial settlement, then the situation can be referred to the Financial Ombudsman. The Financial Ombudsman�s service is free to the customer and they are wholly independent. The Financial Ombudsman�s decision is usually binding on both parties.

The other central piece of protection for the customer is the Financial Services Compensation Scheme. This provides the customer with a level of protection if a financial organisation regulated by the FSA becomes insolvent and cannot properly meet its financial responsibilities to its clients.

Postscript

The above information represents the legal aspects we think you will have found most useful. The information is neither definitive nor exhaustive but is simply an introduction for the layman.

Tinggalkan Balasan