An Executive Perspective by CEO Frenly

Introduction

In an era defined by economic uncertainty, evolving tax regulations, and rising awareness of long-term financial security, life insurance has emerged as one of the most powerful yet often misunderstood financial instruments. Beyond its traditional role of providing protection for loved ones, life insurance today plays a strategic role in wealth preservation, tax efficiency, and comprehensive financial planning.

As CEO of Frenly Financial Group, I have spent decades advising individuals, families, and business owners on how to align protection with opportunity. One topic that consistently draws attention—yet remains insufficiently explained—is life insurance available with tax relief. This article aims to provide a clear, executive-level explanation of how life insurance can deliver not only peace of mind but also meaningful tax advantages when structured correctly.

This is not merely a discussion about products. It is about strategy, foresight, and responsible planning for the future.

Understanding Life Insurance Beyond Protection

Life insurance is commonly perceived as a safety net—something purchased with the hope it will never be needed. While protection is indeed its foundation, modern life insurance has evolved far beyond a simple payout upon death.

Depending on the structure, life insurance can:

- Protect family income and lifestyle

- Support estate planning goals

- Serve as a long-term savings or investment vehicle

- Reduce taxable income or tax exposure

- Provide liquidity at critical life stages

From an executive standpoint, life insurance should not be viewed as an expense, but as a financial asset—one that integrates seamlessly with broader financial and tax planning strategies.

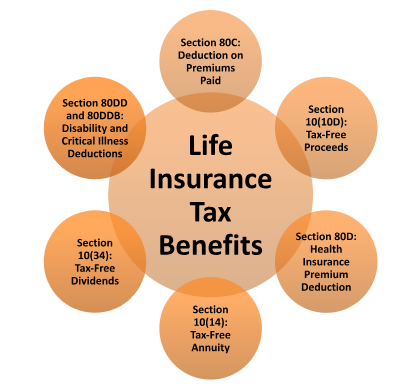

What Does “Tax Relief” Mean in Life Insurance?

Tax relief, in the context of life insurance, refers to legally recognized tax advantages provided by governments to encourage responsible financial planning. These benefits vary by jurisdiction, but generally fall into several categories:

- Tax-deductible premiums (in specific policies or limits)

- Tax-deferred growth of policy cash values

- Tax-free death benefits to beneficiaries

- Reduced estate or inheritance tax exposure

The key is compliance. Tax relief is not about avoidance; it is about using existing laws responsibly and transparently.

Why Governments Encourage Life Insurance

From a policy perspective, governments recognize that individuals who plan responsibly reduce long-term public financial burdens. Life insurance supports this goal by:

- Preventing families from falling into financial distress

- Reducing dependency on social welfare systems

- Encouraging long-term savings discipline

- Supporting intergenerational wealth stability

As a result, many tax systems reward life insurance participation with incentives and reliefs. These incentives are not loopholes—they are deliberate economic tools.

Types of Life Insurance That May Qualify for Tax Relief

Not all life insurance policies are created equal. Understanding the differences is essential.

1. Term Life Insurance

Term life insurance provides coverage for a specific period. While premiums are generally lower, tax relief is usually limited. In some regions, premiums may be deductible when policies are linked to income protection or business purposes.

2. Whole Life Insurance

Whole life policies combine lifelong protection with a savings component. The cash value grows over time, often on a tax-deferred basis. In many jurisdictions, this growth is not taxed annually.

3. Universal and Unit-Linked Life Insurance

These policies offer flexibility and investment exposure. When structured correctly, investment growth within the policy may benefit from tax deferral or favorable tax treatment.

From an executive advisory perspective, these policies are often best suited for long-term planning rather than short-term gains.

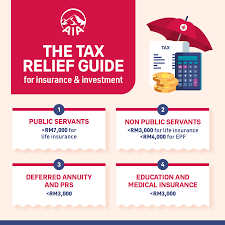

Tax Relief Through Premium Deductions

In certain jurisdictions, life insurance premiums may be deductible up to a specific annual limit, particularly when the policy:

- Is tied to retirement planning

- Covers dependents

- Is mandated within employment or business structures

While limits apply, even modest deductions can create meaningful cumulative tax savings over time.

Tax-Free Death Benefits: A Core Advantage

One of the most universally recognized advantages of life insurance is the tax-free nature of death benefits. In most tax systems:

- Beneficiaries receive payouts without income tax

- Funds are paid quickly, bypassing probate delays

- Financial stability is preserved during emotionally difficult times

For families, this feature alone can represent one of the most efficient wealth-transfer mechanisms available.

Life Insurance in Estate and Inheritance Planning

For high-net-worth individuals, estate taxes can significantly erode wealth. Life insurance provides liquidity exactly when it is needed—at the time of death.

Strategic uses include:

- Paying estate or inheritance taxes without selling assets

- Equalizing inheritance among heirs

- Preserving family businesses or properties

From a CEO’s perspective, life insurance is not optional in estate planning—it is essential.

Business Applications and Executive Tax Efficiency

Life insurance is also a powerful tool for business owners and executives.

Common applications include:

- Key person insurance

- Buy-sell agreements

- Executive compensation planning

- Deferred benefit structures

When structured correctly, these policies may offer tax-deductible premiums for the business, while delivering tax-efficient benefits to executives or shareholders.

Common Misconceptions About Tax Relief and Life Insurance

Despite its advantages, misconceptions persist.

- “Tax relief is guaranteed.” It is not. Eligibility depends on policy type, jurisdiction, and compliance.

- “Life insurance is only for the wealthy.” In reality, tax-efficient policies are accessible at many income levels.

- “It’s too complex.” Complexity is manageable with proper advice.

Education is the antidote to misunderstanding.

Risk Management and Regulatory Compliance

Tax benefits should never be the sole reason for purchasing life insurance. Regulations change, and misuse can result in penalties.

Responsible planning involves:

- Professional advice

- Transparent disclosure

- Regular policy reviews

At Frenly Financial Group, compliance is not a checkbox—it is a core principle.

A CEO’s Framework for Choosing the Right Policy

When advising clients, I recommend a structured approach:

- Define financial goals

- Assess family and business risks

- Understand current and future tax exposure

- Choose appropriate policy types

- Review regularly as laws and circumstances evolve

Life insurance is not static. It must evolve with your life.

The Long-Term Value of Tax-Efficient Protection

The true value of life insurance with tax relief is not measured in annual deductions alone. It is measured in:

- Stability during crisis

- Preservation of dignity

- Protection of legacy

- Confidence in the future

These outcomes cannot be replicated by short-term investments.

Ethical Responsibility in Financial Planning

As financial leaders, we carry an ethical responsibility to guide clients toward sustainable, lawful strategies. Life insurance with tax relief represents a convergence of personal responsibility and public policy alignment.

It is a tool that rewards foresight, discipline, and integrity.

Conclusion: A Strategic Asset, Not a Shortcut

Life insurance available with tax relief is not a loophole, a trend, or a marketing gimmick. It is a strategic financial asset—one that, when used correctly, strengthens families, businesses, and economies.

As CEO of Frenly Financial Group, my message is clear: do not view life insurance solely through the lens of cost. View it through the lens of value, protection, and long-term impact.

The future is uncertain, but preparation does not have to be. With the right strategy, life insurance can provide security today, relief tomorrow, and confidence for generations to come.

Word Count:

501

Summary:

At last you can buy life insurance and get tax relief. The breakthrough results from changes in the Gordon Browns’ latest Budget speech but the tax relief is only available on a new special sort of life insurance policy. You can’t get tax relief on your existing life insurance policies.

These new policies exploit a loophole in the new Finance Bill and should result in savings of between 5% and 15% for standard taxpayers and around 30% for higher taxpayers.

But there are…

Keywords:

life,insurance,tax,relief

Article Body:

At last you can buy life insurance and get tax relief. The breakthrough results from changes in the Gordon Browns’ latest Budget speech but the tax relief is only available on a new special sort of life insurance policy. You can’t get tax relief on your existing life insurance policies.

These new policies exploit a loophole in the new Finance Bill and should result in savings of between 5% and 15% for standard taxpayers and around 30% for higher taxpayers.

But there are strings attached! You can’t add extras on to your life policy such as critical illness cover and the insured sum must be a fixed sum. Neither can you have a joint policy. Basically, it has to be a bog standard, level term, single beneficiary, life insurance policy.

Then there are more restrictions, but quite honestly, these are unlikely to pose a problem to anyone unless they’re very wealthy! You can’t have one of these special life policies if the annual contributions you pay into your pension plus the life insurance premiums, exceed �215,000 per year. Furthermore, if the value of your pension fund plus the payout on your life policy exceeds �1,500,000, the current limit set by the Chancellor, then the excess will be taxed at 55%. Conventional life insurance policies are excluded from this calculation.

Tax relief on the premiums is automatically collected by the life insurance company so you pay a premium which is already reduced by standard rate tax relief. If you’re a higher rate taxpayer, you’ll have to claim the extra tax through your self-assessment tax return. However, once you’ve told your taxman about your premiums, they should automatically continue to give you the tax relief through your tax code.

So why are the savings less than the value of the tax relief? Well, the reason is that the life companies have to administer the tax relief and there are certain operational restrictions imposed by the Inland Revenue on the insurance company. This means that the basic cost of these policies is a little more than conventional life insurance � but after the tax relief you should save.

As with all these loopholes, you must be aware that the Chancellor could remove the tax relief. Having said that, it is rare for a future tax change to be applied retrospectively so you are likely to be safe. Your income could also change and move you into a lower tax bracket. This would reduce your savings.

This new type of life policy is now available from most of the big UK insurers and specialist life insurance brokers. However, you won’t be able to get an online quotation � you’ll have to speak on the phone to a Life Insurance Adviser.

And just to confuse matters these policies are known under a range of names: Pension Term Insurance, Life Insurance with Tax Relief, Life Protection with Tax Relief � but they all mean the same thing.

Oh yes, let me confirm one miss-understanding. No, you don’t have to buy a pension at the same time!

Tinggalkan Balasan